Business Assessment

The Challenge

Evaluating financial flows is essential to observing the life of a business and its ability to generate income. The skills needed for evaluation are multiple and apparent, especially if the company follows the international accounting principles.

Some of the main purposes of evaluation may be: transfer (transfer or merging of a company), liquidation, preparation of financial statements in accordance with the rules of the civil code, transformation of the corporate type, withdrawal or entry of a shareholder.

The steps through which the evaluation work is articulated are as follows:

- Estimation of the discount rate (cost of equity or debt)

- Estimation of current revenues and cash flows of different assets, both for investors and claim holders

- Estimation of future revenue and cash flows of the enterprise that need to be valued, generally estimating the expected growth of earnings

- Estimation of when the company achieves “stable growth” and what features (risks and cash flows) will have

- Choosing the correct DCF template for this activity and evaluating it.

In addition, a prospective and historical analysis is critical in order to estimate the company’s present and future value. Being alongside valued business and legal advisers is a must in order to emerge and to be a step ahead of competition.

The Solution

Eurokleis can take pride in the amount of experience it has regarding financial assessment, utilising various DCF (Discounted Cash Flows) methodologies. The model follows two different assessments depending on whether the value of the capital or of the enterprise is prioritised. The team of experts assists in evaluating companies with critical factors by applying the most appropriate discounting criteria.

We can assist you in your business valuation, and in particular:

- In the assignment or acquisition negotiations, to determine the correct value

- In aggregation or reorganisation processes, for the definition of a trustworthy value

- In measuring periodic business performance for resource optimisation and lowering costs

- In the stock market

Discounted Cash Flow (DCF)

The financial method of Discounted Cash Flow (DCF) is the most accredited by modern business theories, and is particularly well-reputed in assessing individual business areas of the enterprise.

It relates the company’s value to the ability to produce a level of financial flow adequate to meet an investor’s expectation of remuneration.

The DCF method is recommended by the International Accounting Standards (IAS 36) for the valuation of the usefulness of Cash Generating Units (CGUs), which is the smallest set of assets of an enterprise capable of generating cash flows independently in the context of the impairment test (impairment test or impairment test) of the value of individual assets. These are recognised in financial statements (tangible and intangible fixed assets, including those arising from acquisitions, as well as for investments in subsidiaries, associates and joint ventures).

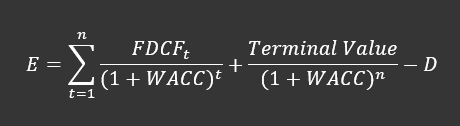

The formula that expresses the value of the company is as follows:

where:

FDCF t = net operating cash flows expected in the explicit forecast period

WACC = discount rate, expressed as the weighted average cost of capital

N = number of years of explicit prediction

Terminal Value = finalised value of the company, corresponding to the current value of the operating flows for years n + 1 onward (ie the period after the explicit provision)

D = net financial position

According to the prevailing practice, the value of a company’s capital is given by the algebraic sum of the following components:

- The present value of net operating cash flows that will be able to generate in the future (in the explicit and the subsequent forecast period, defined as the final value) discounted at a rate equal to the weighted average cost of capital (Weighted Average Cost of Capital or WACC);

- The net financial position (giving the difference between financial debt, financial assets and readily liquidated fixed income securities);

- The market value of any non-typical asset management activities or otherwise not considered for the purposes of projections of surplus assets but not present in the case and not included in the formula

Author of the article

Fabrizio Ausili

senior partner - Tax & Compliance

Chartered Accountant and Accounting Auditor

![]()

You may also be interested in the following articles:

Facilitated Finance: The New Sabatini Law

Access to credit is critical to the company’s competitiveness. New in financial leasing for SMEs and micro-enterprises for the purchase of new machinery, plant and equipment

Business Model Development

A company is only successful if it creates value. Business modeling is therefore essential to effectively manage your business idea.